Link to the original article: https://www.cbinsights.com

In this report, we explore what data is needed to value a company, how to spot undervalued or overvalued businesses, and which valuation methods to use.

Both a science and an art, valuing a business is notoriously hard. But knowing a company’s value is crucial.

Business valuations help venture capital (VC) firms track their portfolio performance, mergers and acquisitions (M&A) teams analyze acquisition targets, and entrepreneurs raise money.

In this report, we explore how to value a company, whether it’s public or private, pre-revenue or post-revenue, overvalued or undervalued.

Table of contents

Selecting a business valuation method

Determining if a company is over or undervalued

- Public filings (S1, IPO, government filings)

- Actuals and estimates (through CBI Dow Jones VentureSource data)

- Whisper valuations

What is a valuation?

Business valuation is the process of calculating the financial value of a company or an asset. The valuation involves collecting and analyzing a range of metrics, such as revenue, profits, and losses, as well as the risks and opportunities a business faces. The goal is to arrive at a company’s estimated intrinsic value and enable entrepreneurs and investors to make informed purchase, sale, or investment decisions.

However, the valuation process is far from being purely scientific. “There is still a huge amount of art involved,” says James Faulkner, managing director at London-based VC firm Vala Capital, “because the financial model [for valuing the company] will depend entirely on subjective inputs: estimates for everything from the rate of sales growth to the company’s salary costs for the next five years.” These assumptions make any valuation an educated guess at best.

Still, the valuation process is important. It helps analysts calculate the intrinsic value of an asset, which sometimes can be detached from its current trading market price. Intrinsic value strives to be objective and less affected by the short-term ups and downs of the economy. The difference between intrinsic and market values is often where profits are made and losses incurred.

CB Insights is one of the only platforms on the market that is able to extract valuation data from public filings. Our platform applies machine learning to calculate and report company valuation. Start your 30-day trial today.

Read on for how valuations factor into CB Insights Company Profiles.

Data used to determine valuations

There are some key pieces of information for determining a business’ valuation:

Financial records. From revenues to costs to debt, having detailed and well-documented financial records allows appraisers to determine future cash flow and profits. Financial data is also vital for calculating growth rates. Startups with high growth prospects tend to receive higher valuations.

The impact of growth rates on revenue. Source: a16z

Management experience. Managers with a strong record of success positively affect a business’ value. But if an entire business’ survival depends solely on its CEO’s unique skill set, investors can’t ignore that risk factor. Employee experience and motivation are equally important — smart, loyal professionals increase the value of a company they work for.

Market conditions. The state of the economy, interest rate levels, and average salaries are other factors to consider. A booming economy could increase demand for specific products and services. However, a sector saturated with many similar businesses may decrease the valuation of new entrants.

Intangible assets. Reputation, trademarks, and customer relations can boost business valuations. Although it’s often hard to put a figure on these assets, their impact is significant.

Tangible assets. Tools, business premises, and vehicles also need to be taken into account, and their value can be easily calculated. Depending on their volume and quality, physical assets can boost business valuations.

Company size. Larger companies typically command larger valuations than their smaller counterparts because of greater income streams. Big businesses also tend to have easier access to capital and well-developed products, and they are less impacted by the loss of key leaders.

Competitive advantage. If this advantage can’t be maintained over time, the business’ valuation will take a hit. But companies that can maintain their competitive advantage for longer periods of time can command higher valuations.

Who uses business valuations?

Different groups need to know how to value a company for different reasons.

Venture capital (VC) firms value companies to be able to report to limited partners (LPs) on how their investments are performing. Knowing the value of companies in which VCs plan to invest is important, too. Valuation data helps investors during negotiations and can inform their decision to ask for liquidation preferences or increased board representation. VCs also need valuation when exiting a business. Having more data helps them get a fair price for equity they plan to sell.

Corporate M&A teams need accurate valuations of companies they plan to invest in or acquire. Many of these acquisition targets are private businesses. Calculating their value is more difficult than valuing public companies, but it’s critical to ensuring each side is satisfied with deal terms.

Investment bankers have to know the valuations of companies they deal with, whether they’re helping clients sell, buy, or invest. Knowing valuations helps bankers provide effective advice. Valuation data is also important for producing industry reports and pitching new clients.

Entrepreneurs use company valuation data extensively. When looking to sell a business, for example, entrepreneurs want to get a fair price for their shares without scaring off potential buyers. Valuations are vital for pitching to investors, too — a well-documented valuation shows an entrepreneur’s credibility and increases the likelihood of securing funding. Entrepreneurs also need valuation data when developing strategic plans, when planning property succession and inheritance, and in many other instances.

Employees with stock options are interested in knowing whether the value of their options is increasing or decreasing. Alternatively, if staff want to buy shares in the company they work for, valuation data can help set a realistic price.

Retail investors who manage their portfolios need access to valuation data to make investment decisions. These individual, nonprofessional investors now make up nearly a quarter of the US stock market. Valuation data helps them diversify their portfolios and better allocate money using brokerage firms, online trading, and robo-advisers.

How to value a company

Market value indicates how much a company is worth according to market participants and investors.

For public companies, market value can be calculated using the stock price. If a company has 100,000 publicly traded shares selling at $50 each, then its value, known as market capitalization, is $5M.

There are different ways to calculate the value of a private company or go beyond market capitalization when valuing public companies. These include:

- DCF Analysis Method: Calculate today’s value of expected future cash flows using a discounted cash flow analysis.

- Multiples Analysis Method: Estimate the value of a company using a multiple of comparable companies.

- Net Book Value Method: Calculate the net book value of tangible and intangible assets.

- Scorecard Valuation Method: Value a startup using average valuations of startups operating within the same sector, stage, and region.

- Venture Capital Method: Calculate a future post-revenue valuation, and then use that figure to arrive at a pre-revenue valuation.

- Berkus Method: Calculate the value of a startup by assigning value of up to $500,000 to different parameters.

- Risk Factor Summation Method: Estimate the value of a pre-revenue startup by scoring 12 risk categories.

Note, however, that figuring out private business valuations is particularly difficult, given limited historical data and unavailable or unaudited financial information.

Methods for post-revenue companies

Valuing private companies with revenue — meaning they have begun to generate sales, and have entered the “post-revenue” stage — is typically done using discounted cash flow (DCF), valuation multiples, or asset valuation methods. These methods can be used independently or in combination to cross-check conclusions.

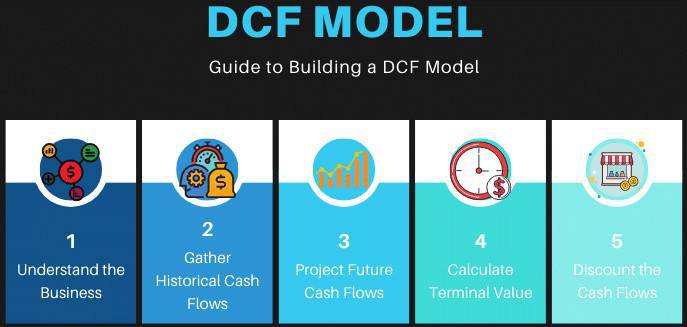

1. DCF Analysis Method

DCF analysis of a company revolves around calculating the future cash flows and discounting them back to today.

Analyzing mature private companies is a straightforward process. They have steady financial data that analysts can use to predict cash flows and compare them with similar public businesses.

Calculating the future cash flows of younger startups is challenging. Many startups are trying to grow as fast as possible, and their cash flow may be nonexistent or limited. Lack of financial data combined with growth-optimized operations make any financial prediction difficult.

In this case, a discount rate is calculated by looking into several different factors:

- Risk-free rate: Channeling money into a risk-free investment, such as a US treasury bond, provides investors with the interest rate known as risk-free rate. Hence, risky investments into private companies need to provide a better return than low-risk alternatives.

- Illiquidity premium: Unlike equities traded on major stock exchanges, private-company ownership can’t be quickly bought or sold. The discount rate is thus higher as investors are “stuck” with their investments for some time.

- Risk premium: Only a small percentage of startups survive beyond a decade of operation. Among those that do, many won’t perform as well as investors hoped. Risk premium is an attempt to capture these risk factors and reflect them in a discount rate.

A summary of steps involved in a DCF valuation method. Source: NYIM

But a DCF valuation method remains imperfect and can be rendered useless with the lack of financial data, prompting investors to look for alternative methods.

2. Multiples Analysis Method

A multiples analysis involves extrapolating the value of a company using a multiple — a ratio calculated by dividing one financial metric (e.g. value) by another (e.g. revenue) — of comparable private companies.

Say, for instance, that owners of a mobile gaming company with $10M in revenue want to price their business. Research shows that several competitors have recently been acquired for 5x revenue. Entrepreneurs can then decide to price their company at $50M.

The difficult part of working with multiples is finding data. Ideally, a mobile gaming company will be compared with firms in the same industry, but that might not always be possible. Comparable firms may not have publicly available revenue figures.

A potential solution is to make a comparison with a broader group of all gaming companies. However, comparing with loosely related businesses makes valuation less accurate.

Factors such as revenue growth and cost of capital can significantly impact multiples analysis. Source: Ad4Ventures

Another challenge is that revenue or profit multiples of comparable companies tend to be static. They only reflect market conditions in a specific period. The mobile gaming company, for instance, may have relied on revenue multiples used in 2015 to calculate its valuation in 2020. But a lot changes in five years.

Also, every company is unique, and knowing revenue without exploring variables such as market growth, staff quality, or profit margins doesn’t tell the whole story.

Some investors use multiples of public companies. But calculating private company valuation by comparing it with public counterparts is an imperfect method, as public businesses are typically larger, more liquid, and less risky.

That’s why startup valuations incorporate a discount to public markets. For example, if a publicly traded software-as-a-service (SaaS) company trades at 8x revenue, the valuation for a similar SaaS startup might use a 6x revenue multiple.

Ultimately, access to private company valuation data is the key to employing a more accurate valuation multiples strategy.

3. Net Book Value Method

Calculating the net book value (NBV) is a valuation method favored by companies with lots of tangible and intangible assets. Tangible assets include land, equipment, business premises, and other physical assets. Intangible assets encompass a range of non-physical assets, such as reputation, patents, and brand.

This method, however, won’t capture the premium the market might place on the company’s value stemming from visionary leaders, growth expectations, etc. As a result, the NBV method tends to yield a lower valuation among methods.

Methods for pre-revenue companies

Valuing pre-revenue startups is more difficult than valuing post-revenue startups because the former lack revenue and profit figures. Hence, pre-revenue valuation is done using a number of imperfect parameters, such as traction, the quality of founders, prototypes, and industry trends.

Traction is an important indicator for many investors. Startups that grow on a small budget, attract customers for a low acquisition cost, and make profit in the process can expect higher valuations.

Investors place a premium on startups with experienced and dedicated founding teams with diverse backgrounds. For instance, having smart programmers as founders is important, but the company will be worth more if the founding team also includes marketers and sales professionals.

Pre-revenue companies can also expect higher valuation if they produce prototypes or minimum viable products (MVPs). A working model of a product shows that a company has the vision and resolve to turn its ideas into reality.

Pre-revenue startup valuation also depends on the market conditions. A saturated market with a lot of competing companies and a limited number of investors will result in lower valuations. But a startup with a valuable patented idea that operates in a booming industry, such as AI or gaming, is likely to be worth more. Investors will find a company particularly appealing if it commands high margins.

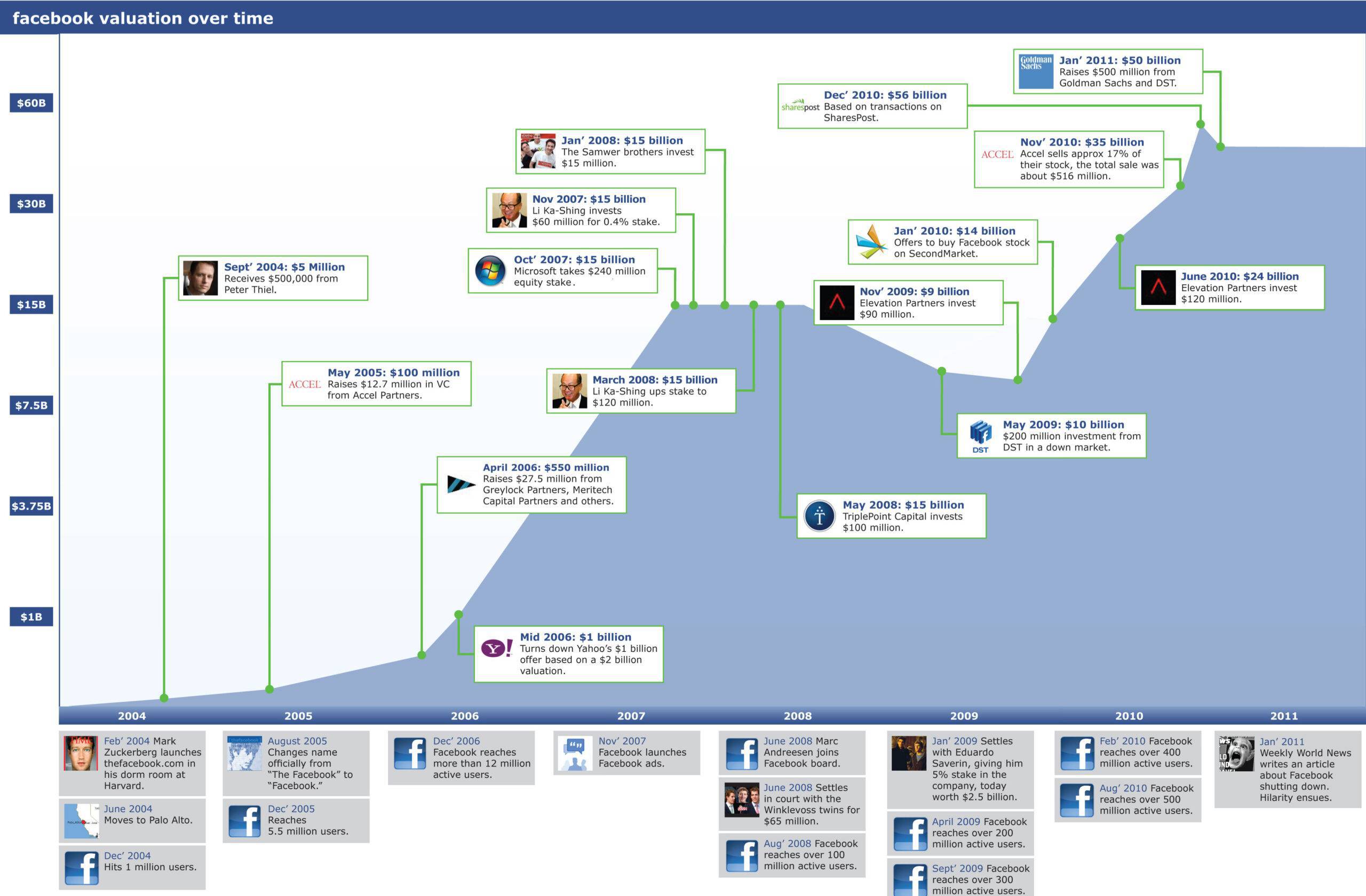

Investing in pre-revenue startups is risky, but potential rewards are immense. Take Facebook: The company’s pre-revenue valuation in 2004, when PayPal co-founder Peter Thiel invested $500,000 into the 4-month-old startup, was around $5M. Today, the company has a market cap of over $700B.

Facebook’s valuation from 2004 to 2011. Source: TechCrunch

Calculating a pre-revenue valuation may seem challenging. But there are several strategies — developed by various investors, entrepreneurs, and academics — that can help.

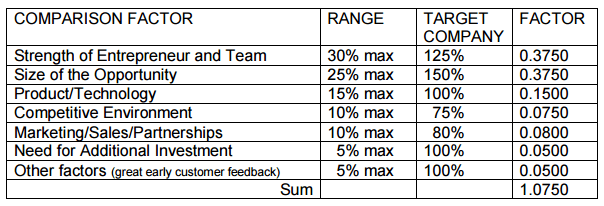

1. Scorecard Valuation Method

The Scorecard Valuation Method, invented by angel investor Bill Payne, compares a startup to other startups that are already funded and operate within the same sector, stage, and region. Several factors are considered, including team, product or technology, competitive environment, sales and marketing, and any need for more financing.

The process starts with finding average valuations of comparable startups. Investors should take into account when these valuation figures were released, because a recession or other market events may have had an impact.

In the next step, investors should apply weights to various factors. Depending on their preferences, some investors may find management teams to be more important than the product. Alternatively, they may value the size of the opportunity more than the efficacy of sales channels.

In the last step, an investor will assign scores to the selected categories. A score of 150% assigned to a management team, for instance, implies that investors find founders and managers of a startup highly competent.

Multiplying the assigned scores with their weights provides the factors.

A scorecard valuation template. Source: humble ventures

Summing up all the factors yields the ratio of the valuation, which is then multiplied by the average pre-revenue valuation of comparable companies. The resulting figure tells us how much a startup is worth. For instance, if a company was assigned a factor of 1.07, and average valuations of comparable startups are $2M, then the company will be valued at $2.14M.

2. Venture Capital Method

The VC Method was developed in 1987 by Bill Sahlman, a professor at Harvard Business School. It involves calculating post-revenue valuation and then using that figure to arrive at a pre-revenue valuation. The future value of an asset is calculated by multiplying projected revenue with projected margin and the industry price-to-earnings (P/E) ratio or another relevant multiple.

For instance, a health tech firm expects a $20M revenue in 10 years, with a 20% profit margin. The industry P/E ratio is 15. So the future value of this business at the year of sale is calculated using the following formula:

$20M * 20% * 15 = $60M

Now, it’s time to calculate the pre-revenue valuation. For that, you need to account for return on investment (ROI) and investment amount. If an investor wants an ROI of 20x on a $1M investment, the following calculation for pre-revenue would apply:

$60M / 20 – $1M = $2M

VC firms and other investors adjust this and other methods to their investment philosophies and approaches. For instance, a metric used by famed VCs like Andreessen Horowitz is average revenue per user (ARPU). VCs can factor in ARPU for comparable companies when calculating the valuation of a pre-revenue company.

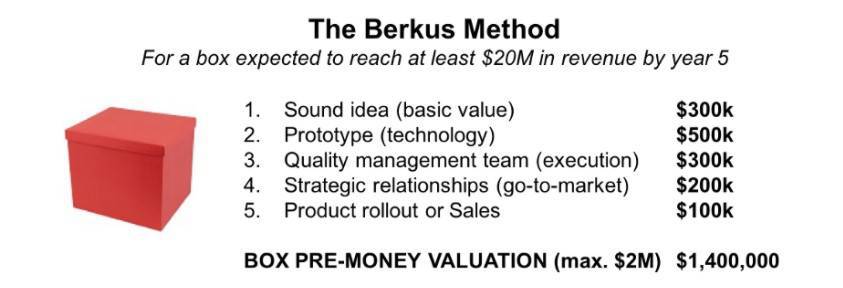

3. Berkus Method

The Berkus Method was invented by angel investor Dave Berkus. It assesses a company’s business idea, prototype, management team, strategic relationships, and sales plan. Each factor can be valued up to $500,000, enabling startups to reach up to $2.5M in valuation.

Source: The PARISOMA Review

The basic idea behind this method is to assign a financial value to risk-reduction elements, but investors can modify this method extensively. If dealing with a medical device startup, for instance, an investor might consider replacing “marketing risk” with “FDA approvals risk,” says Berkus.

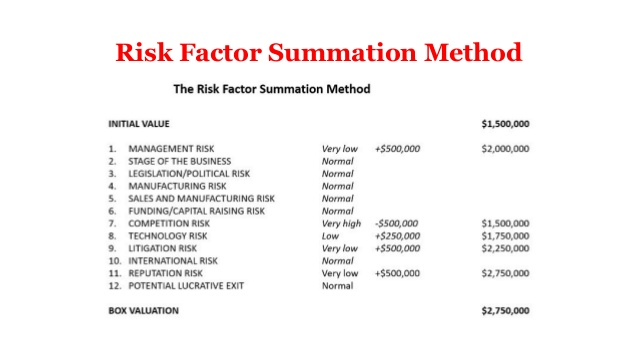

4. Risk Factor Summation Method

This method involves scoring 12 risk categories with ratings from -2 to +2, with negative ratings reducing the final valuation and positive ratings increasing it. In a way, Risk Factor Summation is an extension of the Berkus Method.

Source: Denis Dovgopoliy

Investors score a number of risk categories, including management, stage of business, litigation, reputation, and more. Negative scores can reduce the valuation by up to $500,000, while positive scores increase it by the same amount.

Selecting a business valuation method

There are many business valuation methods to choose from. Some are more complex than others, and different methods may result in different valuations for the same underlying asset.

Selecting an appropriate business valuation method depends on several factors, including the reason you need a valuation. If you’re selling a company, for example, you usually want to achieve a higher valuation. But if you’re acquiring a business, you’re likely to favor a more conservative appraisal to avoid overpaying.

It’s also important to consider whether a company is asset-heavy or service-oriented. If a company is asset-heavy, the net book value method might best capture its value.

Investors also need to know industry norms. Businesses in certain sectors may be typically valued by a specific method or multiples that best capture their value.

Unique characteristics of technologies that companies offer need to be accounted for. A business that pursues exciting but unproven tech might prefer a valuation method that captures future growth potential instead of current assets.

Ultimately, there is no reason not to use multiple valuation methods for the same company and look at the average of all methods.

Determining if a company is over or undervalued

In simple terms, a company is overvalued or undervalued when its market value, evident through market capitalization or VC valuations, is above or below its estimated intrinsic value, respectively.

Calculating this fair value requires undertaking fundamental analysis. Fundamental analysis evaluates company value by studying not only external events but also a range of financial parameters, such as the following:

- Price-to-earnings (P/E) ratio: The ratio between a company’s share price and its earnings per share. A low P/E ratio relative to peers or its historical level might indicate an undervalued company.

- Price/earnings-to-growth (PEG) ratio: A company’s P/E ratio divided by earnings growth rate.

- Price-to-sales (P/S) ratio: The ratio calculated by dividing a company’s share price by the sales/revenue per share. If the P/S ratio is lower than the industry average, the company may be undervalued.

- Dividend yield: The ratio that shows how much companies pay in dividends annually compared with their stock price. Investors like companies with stable dividend yields.

- Earnings yield: The ratio calculated by dividing earnings per share by share price. If a company’s earnings yield is significantly lower than the treasury yield, it may reveal an overvaluation. An earnings yield higher than a treasury yield may indicate undervalued stocks.

- Debt-equity ratio: Calculated by dividing the amount of debt by shareholder equity. A high ratio means a company is more reliant on borrowed money, but the ratio should be compared with the industry average.

- Return on equity: The ratio calculated by dividing net income by shareholder equity. A high return on equity could be one sign investors look for in an undervalued company.

- Current ratio: Calculated by dividing assets by liabilities. If lower than 1, this ratio indicates that a company can’t cover its debts with assets in a short-term period and might be facing financial difficulties.

- Price-to-book (P/B) ratio: Calculated by dividing the stock price by book value per share. If lower than 1, a company’s shares are traded for less than its total assets are worth, signaling potential undervaluation.

Valuation analysis should also take into consideration other factors, such as value traps. Some companies, such as home builders or car manufacturers, enjoy huge profits, low P/E ratio, and large dividends when the economy is doing exceptionally well. But these situations, known as value traps, appear near the end of the economic growth cycle.

What often follows are sharp drops in profit during economic downturns. Blinded by attractive ratios, inexperienced investors may decide to massively invest in these industries, only to be surprised when a market correction kicks in. Value traps aren’t always tied to well-performing businesses, though. Ratios such as P/E are sometimes low because of issues with the business in question.

Examples of overvalued companies

Spotting overvalued businesses on time can save investors a lot of money. Although declaring a company as overvalued is often a subjective stance, we can still observe businesses whose overvaluations were corrected by market forces at a particular point. These include:

Wanda Sports Group: The Beijing-based company, which has partnerships with FIFA and formerly owned Ironman brand, originally wanted to sell over 33M shares for $12-15 a piece in its IPO. But instead of raising $500M as planned, Wanda fell 36% in its Nasdaq trading debut in July 2019, and shares ended up being worth just over $5 each.

The stock kept plunging in the months that followed. It was down 62% by February 2020, forcing the company to sell its Ironman brand for $730M in cash.

WeWork: The office rental and co-working startup went from being valued at $47B to having investors pull their support for an IPO and ousting founder Adam Neumann. The IPO fallout was severe. In November 2019, 2,400 employees lost their jobs. Layoffs were reported in 2020 as well. WeWork had to sell assets, including workplace tech startup Managed by Q and the Lord & Taylor building in New York. Only a bailout from investor SoftBank saved WeWork from collapsing entirely.

In hindsight, the entire catastrophe seemed predictable. In February 2019, 6 months before IPO papers were filed, the company’s price-to-sales ratio was 13.7x. IWG, one of WeWork’s main competitors, had a P/S ratio of 1.4x and was profitable. WeWork also had large debt and mounting losses. Its business model was based on long-term property leases and short-term tenant contracts, making the company’s finances vulnerable to any fall in property rents.

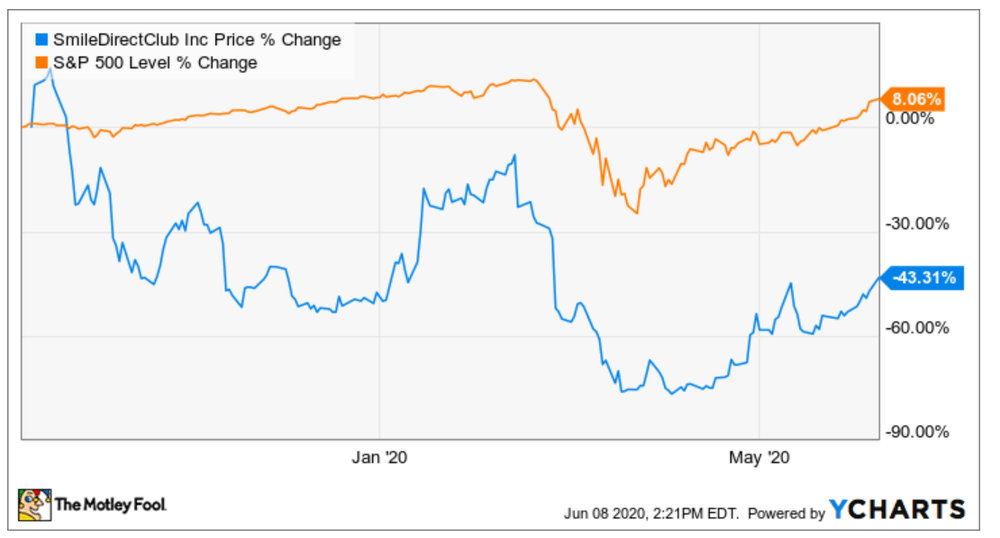

SmileDirectClub: The Nashville-based provider of clear teeth aligners went public in September 2019. The company priced its shares at $23, prompted by an oversubscription to the offering. This price valued the business at $9B, up significantly from the $3.2B valuation reported in its funding round 11 months before. However, share price sank 28% on its first day of trading and closed at under $17.

Shares of SmileDirectClub underperformed compared with S&P 500 levels. Source: The Motley Fool

Further, the Covid-19 pandemic devastated the company’s retail sales channels, and by June 2020, the stock’s price was down 44% since the IPO.

Pets.com: One of the most publicized journeys from IPO to bankruptcy in the dot-com bubble era was Pets.com. Armed with an iconic puppet mascot and catchy slogans, the online pet-supplies seller attracted investors’ attention. Amazon, for instance, owned nearly one third of the company.

In its IPO in February 2000, Pets.com raised $82.5M. The shares opened at $11 and rose to $14 — only to fall to $0.19 within 9 months, when the company announced its bankruptcy.

A series of flaws in its business model brought the business down. For one, Pets.com couldn’t figure out how to economically ship large bags of dog food. Many customers were unwilling to wait for deliveries and preferred to visit local stores and take products home the same day. After 9 months of straight losses, bankruptcy was the only remaining option.

Examples of undervalued companies

Buy low, sell high. That’s the basic logic behind value investing in which investors try to buy stocks priced below their fair value and cash in when shares increase in value. Unsurprisingly, undervalued stocks are in high demand by VC and public market investors.

From Etsy to Facebook to Square, there are many examples where initial skepticism and concerns regarding business models were overplayed. Those companies eventually grew dramatically and delivered great value to their investors.

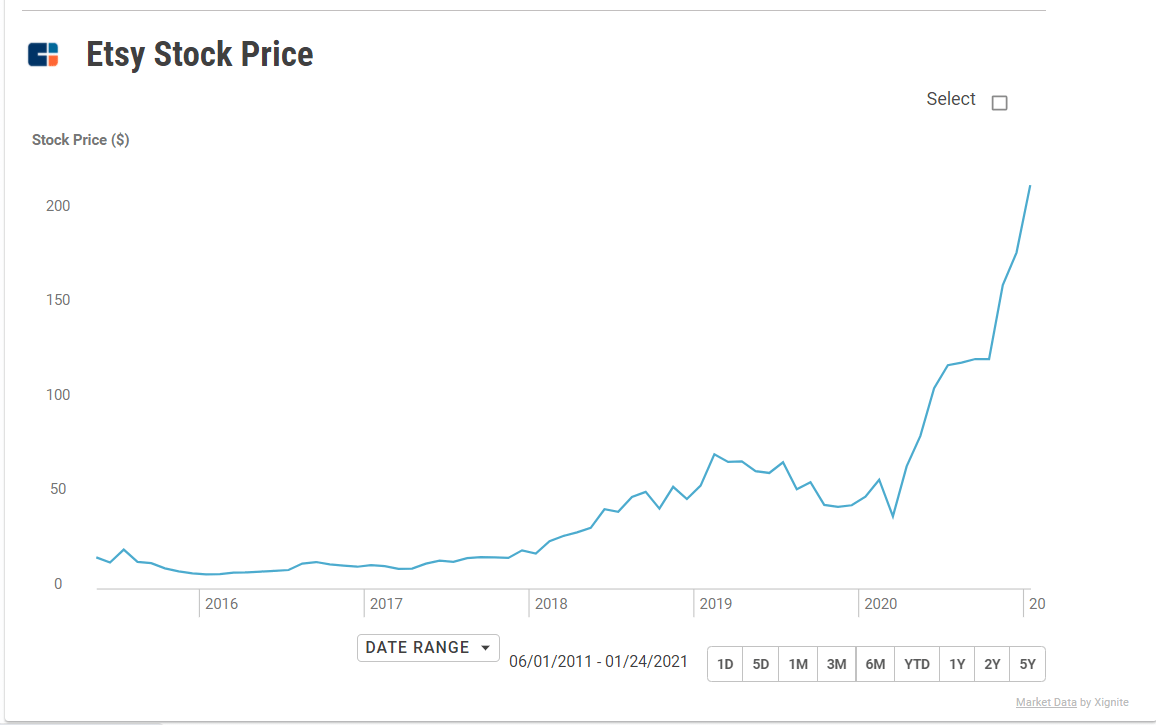

Etsy: The online marketplace company debuted in its 2015 IPO at $31 per share, but within months this had nosedived to below $9. Many questioned whether Etsy could survive in an e-commerce space dominated by the likes of Amazon and eBay. There were also concerns about counterfeit goods: In 2015, a report warned that as many as 2M items sold on the site could violate trademark laws.

But Etsy kept growing its business despite initial skepticism, and these efforts eventually paid off. Between 2015 and 2018, the company’s revenue increased by 120%, the number of active sellers grew by 63%, and positive earnings per share rose to $0.69. Then, in 2020, Etsy’s valuation skyrocketed: Stock price grew to over $170, and revenue in Q3 reached $451M, up from $228M in Q1.

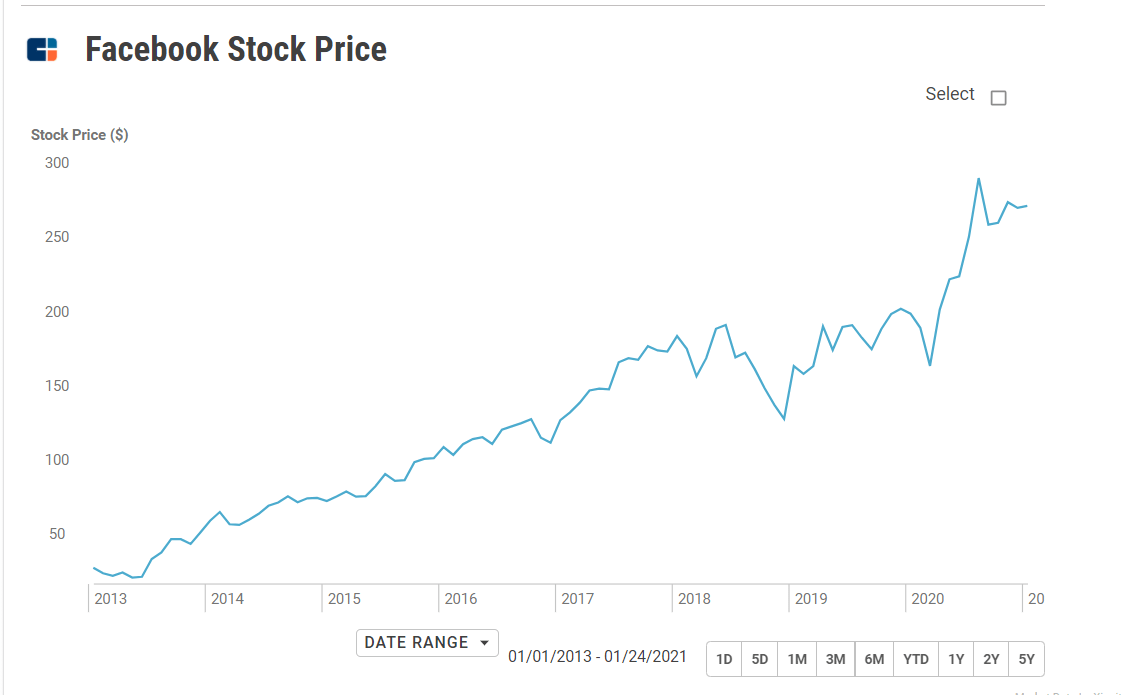

Facebook: The social media giant’s IPO was surrounded with both high expectations and skepticism. Facebook was looking for a valuation of over $100B, which was 108x its annual earnings at the time. For comparison, Google was trading at less than 19x its earnings. Many investors were skeptical, arguing that Facebook would need huge financial growth and new revenue streams to justify its valuation.

The social media company went public in May 2012. Shares initially opened at $38 each but plummeted in the following weeks, wiping out $50B in valuation by August. Since then, however, Facebook has grown immensely.

As of January 2021, the social media behemoth is worth over $700B, trading at more than $250 per share. Revenue in Q3’20 was up 22% year-over-year (YoY). Facebook continues to report strong financial results while navigating multiple political and regulatory challenges, including antitrust suits.

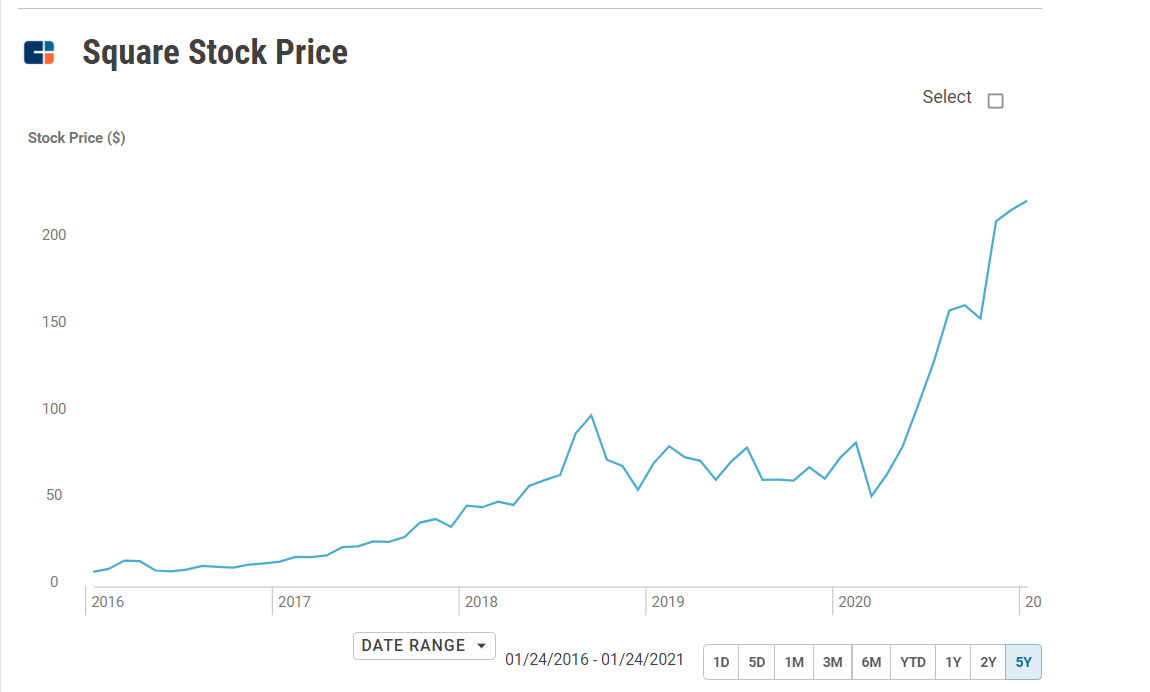

Square: The mobile payments company was valued at $2.9B — down from its $5.3B VC-backed valuation — when it went public in 2015. Investors were hardly convinced that the startup could take on major competitors and achieve profitability.

Square has since recovered and grown immensely, benefiting from the wider adoption of e-commerce and mobile payments. The Covid-19 pandemic has only accelerated this shift.

Square has also ventured into the cryptocurrency sector, allowing its clients to trade bitcoin using the mobile payment service Cash App. In Q3’20, Square reported net revenue at just over $3B, a 140% rise YoY. The company’s market cap increased above $100B with share price reaching over $200 in January 2021.

Where to find valuation data

Business valuations are only as good as the underlying data. But accurate valuation data is in short supply. Investors, analysts, and entrepreneurs thus rely on a broad range of sources to come up with the best educated guess on company values. From S1 documents to whisper figures to public filings, every piece of information is carefully examined.

Public filings (S1, IPO, government filings)

Unlike public companies, private businesses aren’t required to disclose financial statements and information to the public. Hence, finding public or government filings of private businesses is difficult and expensive. Even when possible, it often involves procuring data such as tax estimates, tax returns, and revenue figures from state registries across the US.

In some instances, the taxation agency may possess relevant information. Analysts may also be able to provide estimates on revenue and other financial metrics of large private companies.

S-1 forms can be a valuable source of information on private companies. This form is filed with the US Securities and Exchange Commission (SEC) when a company intends to go public. It contains how much money a company plans to raise and a summary of its business, financial performance, and more.

Investors study these pieces of information to decide whether to buy shares in the company. S-1 documents filed by giants such as Google, Facebook, and Uber are interesting even to non-investors because of a wealth of details on new industries and technologies.

Some businesses prefer the confidential IPO. In this case, the company’s private S-1 form is revealed to the public only 3 weeks before an IPO is scheduled to happen. These companies are in no rush to go public. They can wait for favorable market conditions that will maximize share price without revealing sensitive information to competitors.

Airbnb, for instance, delayed its IPO planned for spring 2020 because the Covid-19 pandemic was wreaking havoc on the hospitality industry. Instead, the company later filed confidential IPO paperwork and went public in December 2020 as its business started to rebound.

Public companies can sometimes provide valuation data relevant for private businesses. For instance, if a private business was acquired by a public company, the latter might disclose details of the deal to investors via SEC filings. Also, a public company that goes private will still have its previous SEC filings publicly available. These can be a helpful source of information.

Actuals and estimates (through CBI Dow Jones VentureSource data)

CB Insights clients have access to more than 100,000 private company valuations with more being added every day.

After CB Insights acquired Dow Jones VentureSource in July 2020, clients are now able to view 2 types of valuations:

- Actuals: Valuation data pulled directly from news releases, public filings, or other official sources.

- Estimates: An estimated valuation based on deal term data and comparable deal information.

With the most recent update to the platform in December 2020, we’ve implemented technology that pulls public filing data to update the platform regularly with new valuations.

These valuations are part of Company Profiles in the CB Insights platform, covering everything you need to know on the company’s financial position, market potential, IP, and more.

Most profiles include:

- Financings and exits

- Investments and acquisitions

- News and regulatory information

- Patents

- Competitors

- Business relationships

- Related CB Insights research

Company profiles also include the company’s Mosaic score, a quantitative framework to measure the overall health and growth potential of private technology companies using non-traditional signals.

We use Mosaic scores, among other factors, when selecting companies for our lists and rankings, such as the Future Unicorns report. Three groups of signals factor into Mosaic:

- Market. The market model assess the number of companies in an industry, the financing and exit momentum in the space, and the overall quality and quantity of investors participating in that industry.

- Money. What’s the financial health of the company? Our money model looks at the burn rate, the quality of investors and syndicate, its financing position relative to industry peers, and more.

- Momentum. This model factors in social media, news/media sentiment, partnerships, and customer base growth. This is evaluated on an absolute and relative basis compared to industry peers.

CB Insights clients use Company Profiles to recommend companies for investments, partnerships, or acquisitions, as well as get an idea of the general momentum of a specific space and elucidate a competitor’s strategy.

Have a company you’re eyeing? Start a 30-day trial today.

Whisper valuations

Whisper numbers, typically circulated on media and websites, are unofficial earnings per share or valuation forecasts that individual investors, analysts, and traders believe companies are likely to report.

Whisper numbers can be used in different ways. For lack of better data, investors can use whisper multiples to approximate the value of certain companies. Unofficial figures can also add value when the consensus forecast varies widely, and investors and traders look for guidance to avoid an earnings surprise. Whisper data can shed light on a market or a company not covered by analysts.

Rumored figures have real-world consequences. For example, a company that beats consensus estimates but falls short of a whisper number can still see its shares take a steep dive if investors purchased the stock using the whisper earnings as their guide. Despite the company performing well compared to the previous quarter, it still disappointed those using other benchmarks of success.

Whisper numbers are yet another tool that investors can consult, but they are far from a guaranteed way of making money or reaching a smart investment decision. Active investors, in particular, may use whisper numbers to make short-term bets. But value investors are more likely to consult more traditional financial parameters when deciding where to channel their money.

Trusting the market

There are many unknown variables and subjective opinions to consider when valuing a company. Will founders be up to the challenge? Are market conditions to remain favorable? How long can a company sustain its competitive advantage?

Lack of data makes valuing private businesses challenging. Without at least some details on financial performance, valuing a company requires making a lot of assumptions. Even with financial data at hand, VC firms and investment bankers still have to decide which valuation method best suits their goals.

For this reason, it can be useful to consult as wide an array of data sources as possible and use best practices established by other investors, analysts, and traders. Each valuation is unique, and involved parties should use strategies that best reflect their interests.

Ultimately, valuations aren’t permanent. They rise and fall depending on a number of circumstances. But as long as companies are delivering value to customers and building quality products, those efforts will eventually translate into higher business valuations. As economist Benjamin Graham has said, “In the short run, the market is a voting machine but in the long run it is a weighing machine.”